A Happy shareholder 😍 Full Year 2025 Results for HRnet Group and Comfort Delgro

- ckcbiz40

- Mar 1

- 6 min read

Its earnings season again, and many of the companies are reporting their results and thankfully most of my companies have performed well.

Today, I wanted to shine the spotlight on 2 companies - The first is a under the radar company but regional HR recruitment powerhouse that I felt deserve more attn, whereas the second is widely known company in Singapore but with an often misunderstood businesses

(1) The under-the-radar company but regional HR recruitment powerhouse that deserve more attention - HRNet Group

HRNet Group is a Singapore-headquartered recruitment and staffing company, founded in 1992 and listed on SGX (CHZ). Many people may not know this under the radar HR company, but do you know that HRnetGroup is the largest Asia-based recruitment agency in Asia Pacific (excluding Japan), with strong presence in Singapore (HQ), China (Shanghai, Beijing, Guangzhou), Hong Kong, Taiwan, South Korea, Malaysia, Thailand, Indonesia, Vietnam etc. ?You can find more info here: HRnetGroup.

HRNet provides:

Professional recruitment (permanent placements, executive search)

Flexible staffing (contract, temp, outsourced staffing)

HR consulting, payroll and workforce solutions

Its clients include multinationals, SMEs, government-linked companies, and over 100 Fortune 500 firms and HRnet operates under multiple brands including:

HRnetOne

PeopleSearch

Recruit Express

RecruitFirst

SearchAsia

PeopleFirst

Disclaimer: I have owned HRNet since 2019 and have been accumulating along the way, with my most recent purchase in Jan 2026 due to the potential I see in them.

They have just released their Full Year 2025 results on 25 Feb 26 here: Investor Relations: Newsroom, and wanted to share some of the positive sparks I see in them:

Overall, I am a happy shareholder of HRNet which has helped me achieve an effective dividend yield (on cost) of 6.5%! While it took 3 years before HRNet (on the positive side we can read it as stable dividends) finally raised their dividends but my patience has paid off, not to mention the shareholder confidence in their business directions, the mgmt and strategy. I'm definitely looking to add more when I have the gunpowder😉

(2) Widely known company in Singapore but with an often misunderstood businesses - Comfort Delgro Group

What comes to one's mind when Comfort Delgro is mentioned? The usual answers I get: "Oh, that taxi company loh!" "I thought they only have taxi business"

"The biggest taxi company in Singapore?"

If you thought Comfort Delgro only operates in Singapore, you will be surprised to know that Comfort Deglro is 1 of the largest land transport conglomerates in the world with fleets of private hire cars, taxi. public bus, private coaches, school buses, metro train network and ambulance fleet, EV charging businesses in Europe, Australia, NZ and China (which I briefly mentioned in my earlier blog post here: Continued... STI ATH (All Time High)! 3 local banks chiong chiong chiong? How? What next for Sporean investors?). Check out their global footprint and diversified businesses spanning 13 countries below:

Remember years ago when Uber was around in Singapore, together with Grab, pple were predicting the demise of Comfort's taxi business, but look at where's Uber now? 🤣 Even Grab is working with Comfort for GrabTaxi. What about autonomous vehicles killing taxi business? No problem, Comfort Delgro disrupts itself first! See below:

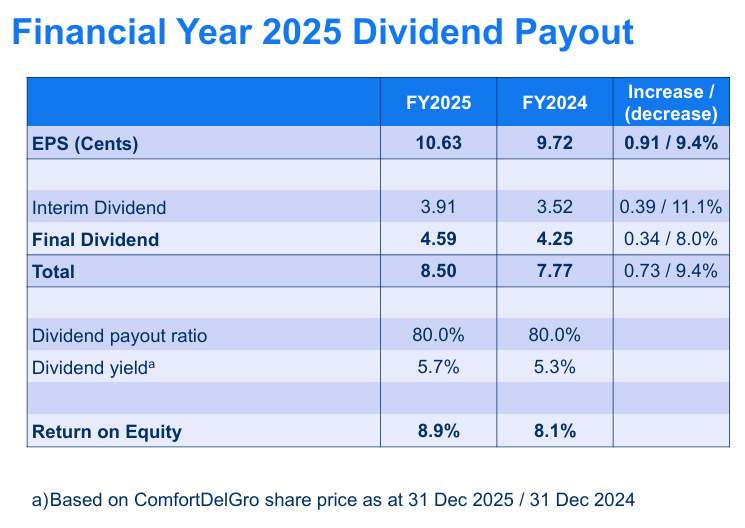

Disclaimer: I have owned Comfort Delgro in my own portfolio since 2020 and yes, I admit that their share price has been stagnant for a while in the past few years. But with the leadership transition and Mgmt's directions and expansion efforts overseas, I see growth in them and in fact I have added it recently into the family portfolio I'm managing and also shared with friends on Comfort Delgro's potential. Alas, my belief has paid off and the giant may have finally woken! Let's see their Full Year 2025 results on 27 Feb 26 and wanted to share some of the bright sparks I see:

If scoring 3 goals in soccer is called a hat trick, Comfort Delgro went above and beyond that with a 4-goal haul in FY2025 for their 4 key business segments below 😍

Did you notice the dividend track record? This is probably the sweetest success as I had forecasted Comfort Delgro is likely to continue growing their dividends as their business expands, and which was why I bought into Comfort Delgro for the family portfolio under management. The latest increase in dividend is validation of my hypothesis and homework 🥰 Now the million-dollar question is whether and when Comfort Delgro dividends may recover to pre-Covid level of 9.79c (see red box)(~15% away from latest 8.5c dividend). In the meantime, 6+% dividend on cost for 1 of the growing land transport giant? Count me in!

To your money and health,

Mr MoneyandHealth (Mr MH) 🥰

Disclaimer: The author is NOT endorsed by any companies mentioned above to write this post. The author may have been, is still vested, will be investing into several of the companies mentioned above. The above article is purely the author expressing his layman views and babbling nonsense, please forgive if it doesn't make sense. The above article is NOT financial advice, and NOT a recommendation to buy or sell any stocks or REITs. Pls do your own due diligence and/or consult a qualified financial advisor before making any moves or taking any actions. Pls note that past performance or track records is not an indicator or guarantee of future performance or potential.

Comments